Biodiversity credits are being promoted as an innovative solution to close the global conservation funding gap (Schwerdtner Manez and Clifton, 2025). The logic seems straightforward: measure biodiversity improvements from conservation or restoration projects, certify them as credits, and sell them to companies wanting to demonstrate their commitment to nature. It’s an approach modelled on carbon markets, which have mobilized billions of dollars for climate mitigation.

But there’s a fundamental problem that most biodiversity credit schemes are glossing over—or worse, actively hiding behind complex methodologies.

In 2024, a diverse team of researchers—conservation biologists, ecologists, and biodiversity policy experts published a paper (Wauchope et al, 2024) with a deceptively simple title: ”What is a unit of nature?”. These are scientists who’ve spent careers studying species, ecosystems, and conservation outcomes. And their answer to their own question is stark: a universal unit of biodiversity doesn’t exist and cannot exist.

The research team, led by Hannah Wauchope, Sophus zu Ermgassen, and Julia Jones, introduces the concept of ”deep uncertainty”—uncertainty that, in their words, ”cannot be known or quantified.” This isn’t uncertainty we can resolve with better technology or more data. It’s fundamental to what biodiversity is.

This finding aligns with recent research on biodiversity credit markets. A comprehensive 2025 study by Sven Wunder and colleagues, analyzing 34 biodiversity credit schemes globally, found that roughly half either use unclear baselines or reward actions rather than measured outcomes. The problem isn’t just technical incompleteness—it’s that biodiversity resists the kind of standardization that markets require. As Wunder’s team notes, biodiversity is ”conventionally considered a public good and is hard to compare across locations and contexts (2025).”

Why Biodiversity Is Different

To understand deep uncertainty, think about carbon credits—the model that biodiversity credits are often compared to. Carbon is relatively straightforward: one tonne of CO₂ has the same climate impact whether it’s emitted in Helsinki or Hong Kong, from a coal plant or a car exhaust. This makes carbon fungible, directly interchangeable. You can credibly say ”preventing one tonne of emissions here offsets one tonne there.”

Biodiversity doesn’t work this way. As both Wauchope and Wunder’s research teams note, measuring biodiversity is fundamentally different from measuring carbon because biodiversity is radically locality dependent. A forest in Finland provides different ecosystem services than a forest in Colombia—different species, different evolutionary histories, different relationships with surrounding landscapes. The ecological ”work” that biodiversity does cannot be separated from where and how it exists.

Wunder and colleagues found that 51.5% of current credit schemes combine species-level and ecosystem-level metrics, attempting to bridge this incommensurability problem. But as they caution, this ”results in hard-to-compare gains across projects globally, thus facilitating more segmented markets.” What looks like methodological sophistication is acknowledging an unsolvable problem: there is no common currency for biodiversity.

Building a Market Without a Currency

Biodiversity credits face deep uncertainty—unclear baselines, questionable outcomes. Yet we need this market for our survival. The 2026 IPBES Business and Biodiversity Assessment confirms it: our failure to value nature has created unprecedented decline, turning biodiversity loss into a critical systemic risk for the global economy. Today, nature has no economic value. We use natural resources without paying for them.

But what if there is no common currency for biodiversity? What if biodiversity itself is the wallet, i.e. the container where all nature-related credits must be held, rather than a tradeable currency?

The complexity is real. Measuring biodiversity and creating credits is fundamentally difficult. Our markets run on simple metrics, KPIs, and standardized values that enable easy transactions. Biodiversity doesn’t fit that model—not yet, possibly not ever.

And yet: most businesses cannot survive without nature. We are in a market transition—a moment when humanity must adapt to nature and build markets on ecological terms, not purely economic ones. This means we have to try.

However, one thing must be clear: this emerging market is not a license to bypass environmental responsibility. High-integrity biodiversity credits must follow a strict mitigation hierarchy. Biodiversity impacts must first be avoided, then minimized, before any restoration or offsetting is even considered.

Only by adhering to this ”avoid-first” principle can we ensure that credits represent genuine ecological gain—not a sophisticated justification for continued nature loss.

The Problem with Baskets

Many emerging biodiversity credit schemes have adopted what’s called a ”basket of metrics” approach. Instead of finding one perfect measure, you monitor five to ten different indicators (species richness, population abundance, habitat condition, water quality) and aggregate them into a single number. If your basket shows 15% improvement, you issue 15 credits per hectare. The Wallacea Trust pioneered this approach, and it’s now been adopted across multiple schemes globally.

This seems elegant. But here’s what Wauchope and colleagues make clear: the basket doesn’t solve the problem of deep uncertainty—it just moves it around. Because now you face a cascade of decisions. Which indicators go in the basket? Why measure one type of biodiversity but not another? Why count certain species but not genetic variation? Why include some ecosystem functions but not others? Then, how do you make them comparable? If one population increases 50% but another declines 10%, how do you combine these measurements? They operate in completely different units with completely different ecological meanings. Next, how much should each indicator matter? Should rare species count more than common ones? Should functional diversity be weighted more heavily than simple species counts? Finally, how do you aggregate them mathematically? Simple average? Weighted average? Some other relationship?

What looks like a technical measurement challenge is actually a series of value judgments. Wunder and colleagues found significant variation in how schemes handle these choices: some use equal weighting across all metrics, others prioritize biodiversity dimensions over threats, and many leave weighting decisions undescribed. The point is stark: there’s no scientifically correct answer to these questions. These are questions about priorities, trade-offs, and what we ultimately care about preserving.

Moving from Theory to Practice: Learnings from Nordic BioBuz

When working with stakeholders who have different views on what biodiversity should be prioritized, we found that simple voting isn’t the answer. Instead, in the Nordic BioBuz project, we used a Value Case Methodology and expert opinions considering all the participating stakeholders and the local community assessments to assign ”weights” to different species based on their relative importance to the ecosystem and the community.

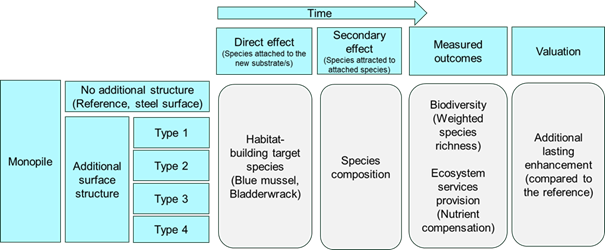

Figure 1. Schematic to illustrate how the concept of biodiversity index and valuation was used in the Nordic BioBuz project.

For example, blue mussels were assigned the highest weight (10) because they are a habitat-building species that creates the functional foundation for dozens of other species to thrive. By using this transparent, expert-led method, we could move from a ”bare steel” reference point to a measured outcome of increased species richness and nutrient removal. This taught us that while the metric might be ”imperfect,” the governance and transparency behind it are what create legitimacy.

Accounting Creates Reality, Not Just Records It

Accounting scholars Peter Miller and Michael Power (2013) show that accounting doesn’t just measure—it shapes what we value and how we organize around it. Biodiversity credit accounting doesn’t merely measure nature; it determines what aspects of nature become visible, valuable, and governable.

When schemes create measurement formulas, they’re not discovering pre-existing units—they’re establishing what counts, literally and figuratively. Every choice about indicators and baselines is both a technical decision and a power structure that defines ecological reality.

This explains Wunder’s findings: only 6% of schemes use rigorous evaluation, and half have unclear baselines (Wunder et al, 2025). These opaque accounting choices create conditions similar to carbon market over-crediting.

Sociologist Donald MacKenzie (2008) showed that financial models don’t just measure markets—they shape them. The same is true here. Biodiversity credit formulas construct a new reality: deciding what counts as valuable, what constitutes improvement, what can be compared. These tools are performative—they create the markets they claim to measure.

The Vision: Building a True Nature Economy

The reality is that we don’t yet have a functioning biocredit market. To get there, we cannot wait for a perfect system to fall from the sky; we must build both credit generation and credit application simultaneously. This is the only way to ensure the high-integrity, robust framework needed to protect the ecological functions we all depend on.

In a true nature economy, economic gain must be derived directly from ecological gain. We might be late to the game, but we simply have to do it. If there is one thing we take with us from the Nordic BioBuz project, it’s that being told your goals are ”too ambitious” is often a prerequisite for success. Had we listened to the skeptics who said it wasn’t possible, we wouldn’t have the results we see today – moving the finish line one blue mussel at a time.

Methodologies will only become more accurate as we get more projects into the water, the forests, and the meadows. But these projects will never start if they are stopped before they are even demonstrated, or if we are constantly questioned for simply wanting to do something good.

We don’t have all the answers yet, but we have the eagerness to learn along the way. The logical next step is a vision that shifts the perspective:

”The shift from credit generation to application requires establishing credits as ’core ingredients’ in sustainability strategies and ’dark-green’ products, while seeking ’ecological interoperability’ to lower administrative costs and transform businesses from passive observers into active facilitators of restoration.(Nordic Biobuz)”

This is how we close the $700 billion annual biodiversity financing gap , tapping into a $130 trillion global economy to prove that restoring nature is not just a moral obligation, but a viable economic activity. We must shift the $4.9 trillion in annual private finance flows that currently directly impact nature negatively—a figure twenty times larger than the amount currently directed toward conservation.

Finally, the uncertainty is real, but so are the ecosystems being restored. The question isn’t whether we can measure biodiversity with precision, because we can’t. The question is: who decides what to measure, and how are they held accountable?

This is where credits become either genuine restoration tools or sophisticated greenwashing. The difference lies not in better metrics, but in better governance around imperfect ones.

We have the resources and the will to make this market transition, but it must be built on high-integrity foundations. This requires a strict adherence to the mitigation hierarchy—where avoiding and minimizing harm is the non-negotiable first step—and a commitment to rigorous third-party verification of transparent, evidence-based projects. By creating a regenerative nature market where economic gain is derived directly from ecological gain, we ensure that the ecosystems we depend on are no longer invisible to the balance sheet.

_ _ _ _

Tomas Träskman, Principal Lecturer Accountability and Sustainability, Arcada

Joel Lindholm, CEO, Under Ytan

_ _ _ _

Refrences

MacKenzie, D. (2008). An engine, not a camera: How financial models shape markets. MIT Press.

Miller, P., & Power, M. (2013). Accounting, organizing, and economizing: Connecting accounting research and organization theory. Academy of Management Annals, 7(1), 557–605. https://doi.org/10.1080/19416520.2013.783668

Schwerdtner Manez, K., & Clifton, J. (2025). Biodiversity credits: A new currency to support nature conservation? Oryx, 59(3), 319–324. https://doi.org/10.1017/S0030605324001467

Wauchope, H. S., zu Ermgassen, S. O. S. E., Jones, J. P. G., Cornforth, H., Bruil, H. S. t., & Milner-Gulland, E. J. (2024). What is a unit of nature? Measuring biodiversity for biodiversity credits. Proceedings of the Royal Society B: Biological Sciences, 291(2353), 20242353. https://doi.org/10.1098/rspb.2024.2353

Wunder, S., Kaczan, D., Naeem, S., Benavides, J. A., Brancalion, P. H. S., Bull, J. W., Calmon, M., Castellanos-Navarrete, A., Chazdon, R. L., Dehm, J., Edwards, D. P., Fisher, B., Freckleton, R., Galik, C. S., Holl, K. D., Meyfroidt, P., Morgans, C. L., Nuñez, M. A., Sills, E. O., … zu Ermgassen, S. O. S. E. (2025). Biodiversity credits: An overview of the current state, future opportunities, and potential pitfalls. Business Strategy and the Environment, 34(1), 8470–8499. https://doi.org/10.1002/bse.4070

IPBES (2026). Summary for Policymakers of the Methodological Assessment Report on the Impact and Dependence of Business on Biodiversity and Nature’s Contributions to People. Jones M., Polasky S., Rueda X., Brooks S., Carter Ingram J., Egoh B. N., von Hase A., Kohsaka R., Kulak M., Leach K., Loyola R., Mandle L., Rodriguez-Osuna V., Schaafsma M. and Sonter L. J. (eds.). IPBES secretariat, Bonn, Germany. DOI: https://doi.org/10.5281/zenodo.15369060.